Turkey-Risk Model Shows Nation’s Markets Going From Bad to Worse

EghtesadOnline: Turkey’s failed coup and President Recep Tayyip Erdogan’s crackdown could hardly have come at a worse time for investors worried about the riskiness of the country’s bonds. Now they may get even dicier.

Even before rogue generals tried to seize control on July 15, the country had a relatively high default probability. It was greater than about 80 percent of nations, according to Bloomberg’s sovereign risk model, which uses debt, currency reserves and political instability metrics to calculate such odds, reports Bloomberg.

“There’s nothing in these factors that will not get worse,” said Salman Ahmed, the London-based chief strategist at Lombard Odier Asset Management, which uses similar gauges to assess government bonds and is staying underweight on Turkey’s debt. “Political risk is going to go up, growth will go down and external debt will go up as a percent of GDP.”

S&P Global Ratings’ post-coup downgrade of Turkey -- and a threat by Moody’s Investors Service to do likewise -- helped stoke a debt selloff. Bloomberg’s index of the country’s sovereign bonds fell as much as 5.2 percent, the most in three years, before rebounding slightly.

Turkey said in January it plans to raise as much as $4.5 billion from international capital markets this year, of which it has so far borrowed $3 billion.

Underperforming Bonds

The government’s borrowing costs, as measured by the premium investors demand over U.S. Treasuries, have now risen to near parity with the global emerging-markets average. They haven’t been at the same level since 2008. The weakening lira, which reached a record low on July 20 as forward markets signaled further declines, will only make borrowing pricier.

“We expect the bonds to continue to underperform the rest of emerging markets,” said Stephen Bailey-Smith, who helps manage $3.2 billion in such securities at Global Evolution Fonds A/S in Denmark. The coup’s “failure supports a more totalitarian government and an increase in tensions and security risk,” he said.

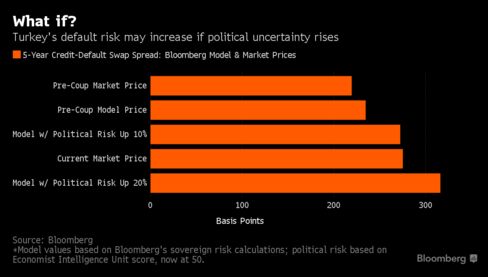

The Bloomberg model uses the Economist Intelligence Unit’s political risk score, which was 50 for Turkey as of June 30, the midpoint of the scale. Bailey-Smith and Ahmed predict the coup will increase political risk. If its EIU score climbs 10 percent, Turkey’s model-implied CDS spread would increase to 272 basis points, near the current market price of 275. An EIU score of 60, still less than after the last military coup in 1997, would imply a spread of 316.

That assumes the model’s other variables remain unchanged, which Lombard Odier’s Ahmed said is unlikely. The model’s current estimate for economic growth of 3.5 percent a year is in line with forecasts. But economic expansion slowed in the first quarter, and the two economists that have updated their predictions since the coup both see weaker growth, one as low as 2.7 percent.

Debt Issue

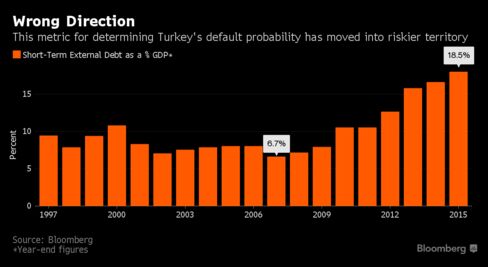

Ahmed said he’s worried about Turkey’s financing of its short-term external debt because “the market may make it difficult for them,” he said. The country’s short-term external debt as a percentage of gross domestic product, one of the measures Bloomberg uses to calculate default probabilities, was trending into riskier territory even before the current turmoil.

Debt with an original maturity of a year or less has almost tripled to more than 18 percent of the economy since 2007. Among eight emerging-market countries that rank just above and below Turkey for default risk, the average is less than 8 percent of GDP with none higher than 12 percent. If Turkey’s level increases at the average of the past four years, it will top 20 percent in 2016.

Turkey’s 12-month forward debt obligations soared to a record 30 percent of economic output at the end of 2015, having risen for four years from 19 percent, data compiled by Bloomberg show.

S&P pointed to similar statistics in explaining its downgrade of Turkey. The country’s net foreign exchange reserves of an estimated $32 billion cover only about two months of current-account payments, giving it little room to maneuver, the firm said. Turkey will likely have to roll over about 42 percent of its external debt, more than $170 billion worth, in the next year, and political instability makes promised reforms to reduce dependence on foreign financing unlikely, S&P said.