China’s Central Bank Chief Warns of ‘Sudden, Contagious and Hazardous’ Financial Risks

EghtesadOnline: China’s financial system is becoming significantly more vulnerable due to high leverage, according to central bank governor Zhou Xiaochuan, who has made a series of blunt warnings in recent weeks about debt levels in the world’s second-largest economy.

Latent risks are accumulating, including some that are “hidden, complex, sudden, contagious and hazardous,” even as the overall health of the financial system remains good, Zhou wrote in a lengthy article published on the People’s Bank of China’s website late Saturday.

The nation should toughen regulation and let markets serve the real economy better, according to Zhou. The government should also open up markets by relaxing capital controls and reducing restrictions on non-Chinese financial institutions that want to operate on the mainland, he wrote.

“High leverage is the ultimate origin of macro financial vulnerability,” wrote Zhou, 69, who is widely expected to retire soon after a record 15-year tenure. “In sectors of the real economy, this is reflected as excessive debt, and in the financial system, this is reflected as credit that has been expanding too quickly.”

The latest in a string of pro-deleveraging rhetoric from the PBOC, Zhou’s comments were speculated to have contributed to a rout in Hong Kong shares. They signal policy makers remain committed to the campaign to reduce borrowing levels across China’s economy. Concern that regulators may intensify this drive after last month’s twice-a-decade Communist Party congress helped push yields on 10-year sovereign bonds to a three-year high, Bloomberg reported.

Chinese bonds seemed to shrug off the essay early Monday, with 10-year yields down one basis point to 3.88 percent as of 11:14 a.m. in Shanghai, while the cost on five-year notes rose one basis point to 3.95 percent. Hong Kong’s Hang Seng Index slumped the most in two weeks and the Shanghai Composite Index fell for a third day in a row.

“Investors are very sensitive to any negative news since the market is at a high level,” said Ben Kwong, executive director at KGI Asia Ltd. in Hong Kong, referring to the equity move. “Zhou’s comment about financial risks are hurting sentiment.”

The PBOC chief’s essay reads more like an explanation of existing priorities than a sign they’re changing direction or pace, said Bloomberg Intelligence economists Tom Orlik and Fielding Chen. China may shift slightly toward a tighter stance, but macro-prudential rather than monetary policy will do the leg work to limit financial risks, they wrote in a note.

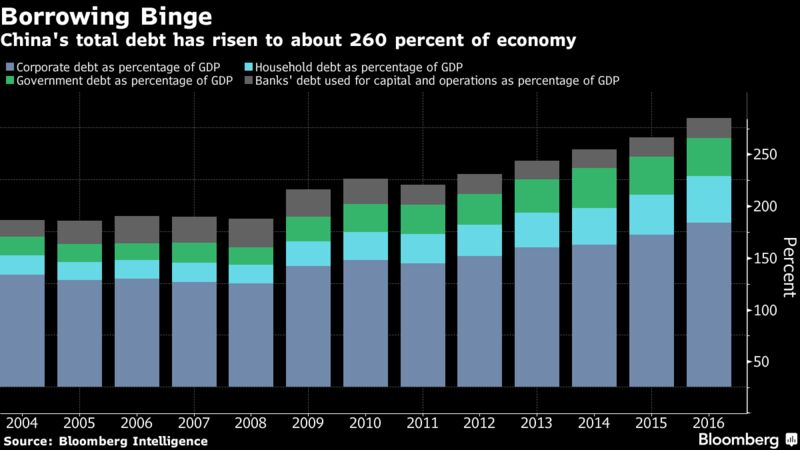

Despite the tough rhetoric around deleveraging in China, measures of credit continue to show expansion, with aggregate financing surging to a six-month high of 1.82 trillion yuan ($274 billion) in September. Corporate debt surged to 159 percent of the economy in 2016, compared with 104 percent 10 years ago, while overall borrowing climbed to 260 percent.

Zhou’s article was included in a book that was published recently to help the public and party members better comprehend the spirit of the 19th party congress, according to the official Xinhua news agency and information on the PBOC’s website.

Here are some of the other points Zhou made:

On risks and regulation

- China’s financial system faces domestic and overseas pressures; structural imbalance is a serious problem and regulations are frequently violated

- Some state-owned enterprises face severe debt risks, the problem of "zombie companies" is being solved slowly, and some local governments are adding leverage

- Financial institutions are not competitive and pricing of risk is weak; the financial system cannot soothe herd behaviors, asset bubbles and risks by itself

- Some high-risk activities are creating market bubbles under the cover of "financial innovation"

- More companies have been defaulting on bonds, and issuance has been slowing; credit risks are impacting the public’s and even foreigners’ confidence in China’s financial health

- Some Internet companies that claim to help people access finance are actually Ponzi schemes; and some regulators are too close to the firms and people they are supposed to oversee

- China’s financial regulation lags behind international standards and focuses too much on fostering certain industries; there’s a lack of clarity in what central and regional government should be responsible for, so some activities are not well regulated

- China should increase direct financing as well as expand the bond market; reduce intervention in the equity market and reform the initial public offering system; pursue yuan internationalization and capital account convertibility

- China should let the market play a decisive role in the allocation of financial resources, and reduce the distortion effect of any intervention

- China should improve coordination among financial regulators