American Shale Companies' Rush to Hedge Is Turning the Oil Market Upside Down

EghtesadOnline: U.S. shale oil companies are using the post-OPEC rally to hedge their oil price risk for next year and 2018 above $50 a barrel, bankers, merchants and brokers said, pushing the forward oil curve upside down.

The rush to hedge -- locking in future cash flows and sales prices -- could translate into higher U.S. oil production next year, offsetting the first output cut by the Organization of Petroleum Exporting Countries in eight years. As such, the producer group could end up throwing a life-line to a sector it once tried to crush, Bloomberg reported.

“Right after OPEC, U.S. producers were very active hedging," said Ben Freeman, founder of HudsonField LLC, a boutique oil merchant with offices in New York and Houston. "We are going to see a significant amount of producer hedging at this levels."

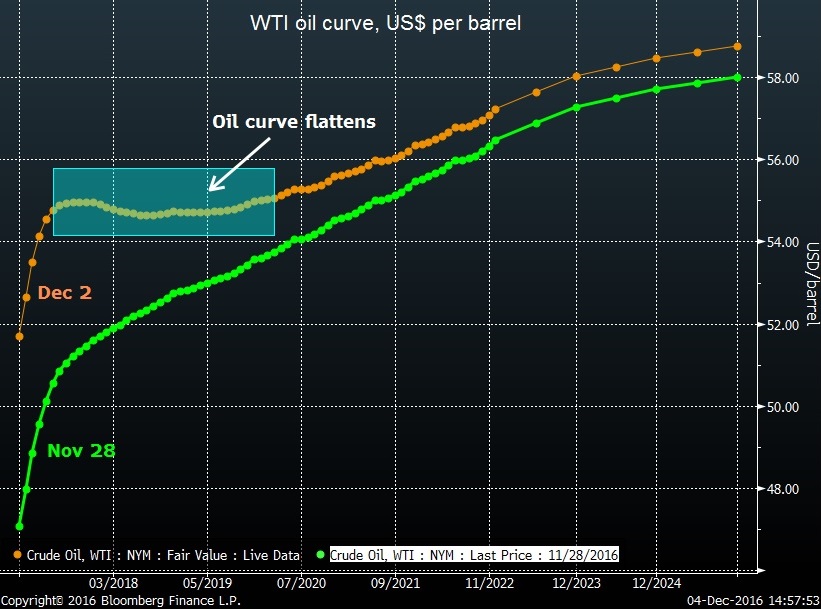

The hedging pressure triggered violent movements across the price curve. As shale firms sold oil for delivery next year and early 2018, the shape of the curve flattened. "The curve is screaming producer hedging," said Adam Ritchie, founder of consultant AR Oil Consulting and a former trading executive at Caltex Australia Ltd. and Royal Dutch Shell Plc.

West Texas Intermediate crude for delivery in December 2017 is now more expensive than in June 2018 -- a condition known as backwardation. A week ago, the forward curve was in the opposite shape, known as contango.

“The longer dated flattening in the futures curve does indeed reflect to a large extent increased producers activity, hedging on the back of the pop up in spot prices that followed the announcement of an output cut by OPEC,” said Harry Tchilinguirian, head of commodity strategy at BNP Paribas SA.

Across the U.S. oil sector, companies pounced. Take Warwick Energy Investment Group. The privately-held owner of stakes in thousands of U.S. wells added hedges on Dec. 1 and 2, immediately after OPEC announced its production cut, according to Katherine Richard, chief executive officer at the Oklahoma City-based company.

“I have over 200 wells currently drilling and I want to lock in my 20 percent-plus internal rate of return,” Richard said. “I hedge to lock in the prices that undergirded my drilling approval decisions."

The latest surge in prices extends U.S. shale drillers’ pattern of adding hedges when crude rises into the mid-$50s. Pioneer Natural Resources Co., for example, said in early November that it increased its hedges for next year to 75 percent of production from 50 percent. In the third quarter, Devon Energy Corp. more than quadrupled its 2017 positions from the prior three months.

WTI oil prices gained 12 percent last week -- the biggest weekly gain in almost six years -- after OPEC announced its cut and Russia promised to reduce output too. WTI ended Friday at a 17-month high of $51.68 a barrel. It rose as high as $52.42 Monday.

U.S. shale companies and other independent exploration and production companies usually reveal their level of hedging with a quarter delay. Nonetheless, anecdotal pricing activity already suggests their presence in the market. U.S.-based oil bankers and brokers also said they handled significant volumes after OPEC agreed to cut production.

A record 580,000 crude options contracts traded on the New York Mercantile Exchange that day, while the number of puts -- used by producers to guarantee a minimum price -- hit the highest since 2012.

As the oil curve flipped, inter-month spreads, which move about 5 to 10 cents a day in normal times, swung eight times as much. The spread between December 2017 and December 2018 -- a popular trade known in the industry as “Dec-Red-Dec” -- jumped from minus $1.35 a barrel early on Wednesday before OPEC announced the deal, to plus 49 cents on Friday.

Another factor keeping pressure on forwards prices is doubt about whether OPEC and Russia will continue to curb supply when the deal ends in six months.

“Two things might be priced in this change -- the first one is that shale producers are hedging and the second one is that the deal is for six months and then no one knows what’s going to happen,” said Tamas Varga, analyst at brokerage PVM Oil Associates Ltd.